A drop in the ocean

Building 1517.

Last week I had the pleasure of sharing our journey at 1517 with emerging managers through the Materials Change program run by the one and only Eve Blossom.

One of the blessings of speaking to groups, and coming back for new cohorts, is that you get to reflect on where things were in the past, the context of those changes, and have a moment to breathe and think about what’s coming ahead.

The context for this class is that we’ve been back in market fundraising for 1517 and the class, unlike most of my presentations, is not geared at startup founders and makers, but investors just starting their funds and getting into firm building. As fund managers starting out, I can see that they are like me, not from pedigreed institutions, excited about founders they want to serve, and always learning. As outsiders breaking in, our story resonates and offers hope on the journey ahead and some lessons learned along the way.

Like everyone in tech, I’ve started using new tools. Granola analyzed and took notes of my talk. Sometimes at 1517 we say we’re a little bit Amish (except the Amish are far far cooler — thank you for building houses in North Carolina!). So, this was also the first time that it dawned on me that I could ask Granola to generate an article.

Like using filters on photos (which I don’t do — real matters) I think disclosure of tool use is important. Below is my story, Granola’s AI gnomes doing their thing, and my revisions and edits (as I am 5 hours into a 16 hour flight to Singapore with no wifi — inbox zero and X will wait).

Maybe this is a bit like when a painter makes prints of their painting, but takes the time to make some accents in acrylics. Or not.

Begin the beguine

I didn’t grow up thinking I’d be an investor. I thought I’d be an educator, forever. My first “startup” was Innovations Academy, a charter school in San Diego, that we opened to 120 students in 2008. Families were losing their homes, the stock market was tanking, and we were entering the Great Recession. I was 28 and blissfully unaware of global macro anything. Gas was expensive, parents struggled to drive to our first location, and I learned, in hindsight, that macro currents carry, or hinder, you whether you notice them or not.

That through line of mission first, resources second, and learn fast, has guided me from alternative education into venture. And make no mistakes, my work is still in education; building environments where talented people can do their life’s work sooner, with fewer gatekeepers, and with resources earlier on.

The Fellowship That Changed Everything

In 2010 I found myself in the Bay Area after moving for love. No job and unsure of my future, I got an unexpected phone call that would change my life from Lindy Fishburne, a director of the Thiel Foundation.

“They’ve lost their minds. They’re starting this new program and they have no one running it.”

The Thiel Fellowship, now nearing normal on its message, was a truly “radical rethinking of what it takes to succeed” (our original motto) focused on younger Millennials. Now in their later teens and on the cusp of Gen Z, this generation of children were coming into abstract thinking during September 11th, as late teens their families struggled through the financial crisis in 2008, and they were coming out of two terms with George W. Bush and were first time voters, largely bringing in the Obama era starting in 2009.

And here we were, in 2010, with $100K grant for those 19 and under to work on projects—research, nonprofits, startups—outside the college path. It wasn’t an accelerator. It wasn’t even about companies. It was about agency. Given everything these young people had been through in our country and how systems had duped them and their families over and over again, agency was a very powerful (and in the eye’s of the authorities, a very dangerous) message.

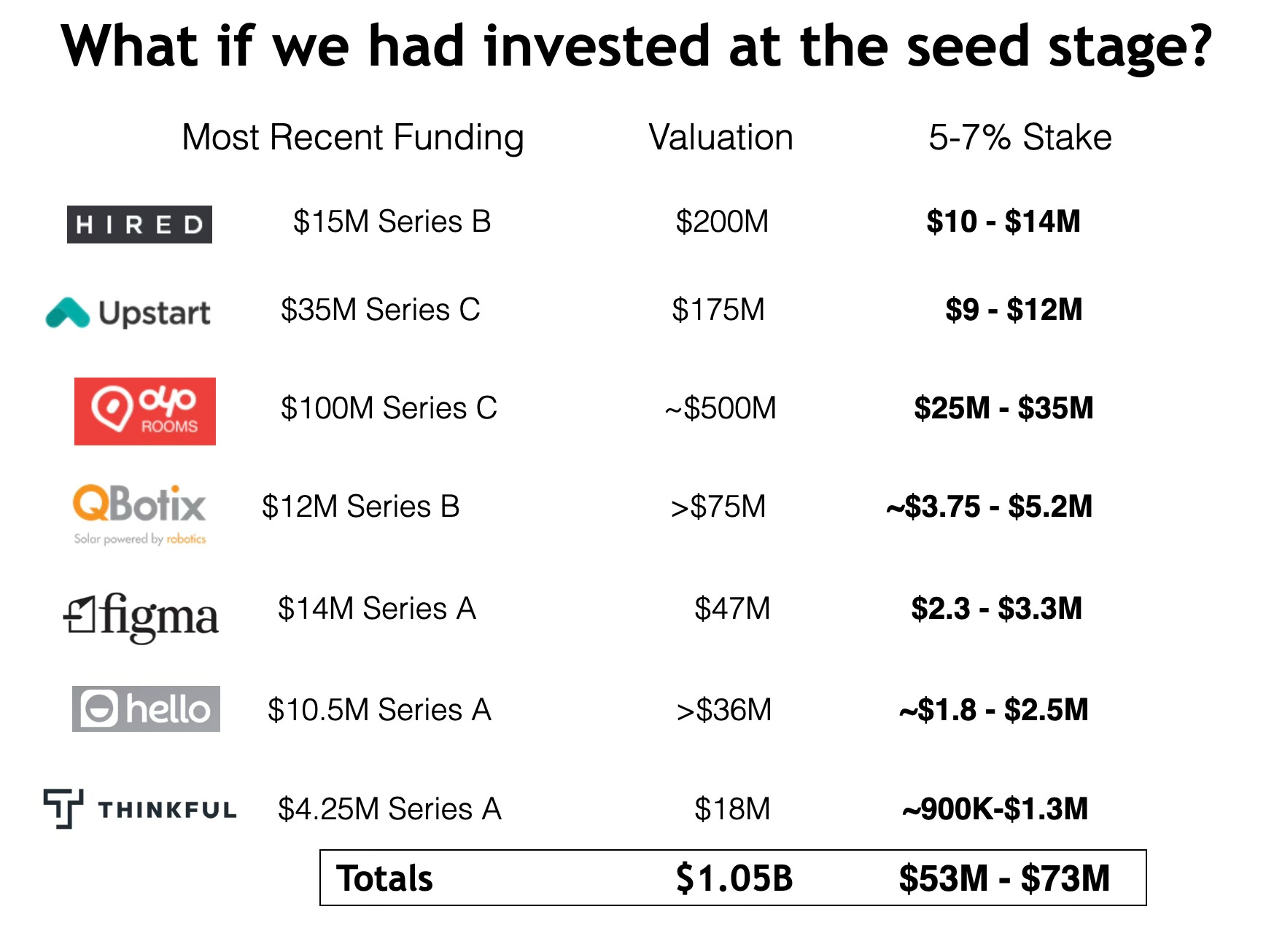

We worked with and funded people like Dylan Field, whose mission (impressively, because pivots are so common, both then and now) was to spark creativity for everyone. Over the summer, and 12 years in the making, Figma IPO’d and Dylan is celebrating the past and current team at Figma as they usher the company into the public eye. Vitalik Buterin launched Ethereum during his fellowship, Laura Deming made advances in longevity funding (and therefor research and outcomes in the space), and Ritesh Agarwal launched and built OYO into one of the largest hotel networks in the world. These weren’t “picks” so much as seeds…acorns to oaks, as we say at 1517. A two-year grant with a ten-year timeline.

But we saw a real challenge during the early days of the fellowship: Silicon Valley reports to love young talent, but most of that love translates to “come work at my portfolio company,” not “I’ll back you.” The tides are changing now, which I am so thankful to see, but even when the first inklings of 1517 were coming together, “real” investors wouldn’t take meetings with fellows to offer feedback on a deck. We were still a “cute program.” Real investing happens elsewhere.

So we became the “elsewhere.”

Becoming Investors (The Great Heist!)

In 2015, my cofounder Michael and I pitched Peter Thiel at breakfast. No agenda — we were going for a genuine surprise attack. But I was terrified. You can take the girl out of New England, but you can’t take the New Englander out of the girl. Going to one’s boss to ask for a blessing to leave was sacrilegious. I might as well have shown up with my own obituary.

Even though I had already lived in California for 12 years, old habits die hard. And though I thought we would be surprising Peter, we were the most surprised. The tables turned, from my Protestant work ethic expectations, a total 180.

We shared a one-pager of a hypothetical track record: what if the fellowship’s $100k grants had been investments? It was clear that the 8 outperforming startups (Figma and OYO included) from the fellowship in 2015 had promising return potential on paper. And more so, that we were accelerating lighting the paper belt on fire more directly by spearheading a movement where we could support more people.

Peter was excited:

“How much are you going to raise?”

“$10M”

The wheels were put in motion. Peter looked down at the floor. The silence was long and Peter was making this particular wince when he’s thinking. I’d like to think that he was doing some intricate calculus, but maybe he was thinking about the fall of Rome.

“You should raise $15M and I’ll be 4 of it.” He said matter of factly but with some extra pep.

My New England brain short-circuited and I smiled so big that I literally covered my mouth with my hands. Could I show him that I was this happy? That it was this much of a surprise to ask for his blessing to leave our roles, only to walk out with more money than I had ever seen on a spreadsheet? We left breakfast, the front door closed and we high-fived like we’d pulled off a heist.

HNWI, Family Offices and Institutionals, Oh My!

Leaving that meeting, we had $4M in the pocket and $11M more to raise. But who did funds raise from? We asked our friends…

We wrote 300 individualized emails—no BCC blast—containing a short blurb and a very very homemade deck. The ask was simple: “Is there anyone we should talk to?” (not, “will you give us money?”). People opened doors. Some said, “Talk to me.” A few advised that family offices, the creators of previous wealth, often with wily starting stories like our Thiel Fellows, would be a good fit. People kindly made intros on our behalf. And those conversations turned into commitments.

It turned out that family offices were a great fit for us and that remains true today. It’s joyful to create additional wealth for families and people where we can see the direct effect of our work and share a long term vision and values.

From our friends, advisors, and mentors, we got some great advice along the way:

A piece of tactical advice from an old boyfriend’s dad became gospel: double the minimum check size in your deck—people negotiate you down by half. He was right every time.

Another potential limited partner (LP, the investors in a fund) asked to see us make two investments before committing. Between us, we had about $150K in savings and the fund wasn’t formed yet, so we warehoused two checks personally— bye bye savings. One went to a company that later died. The other went into Fountain, now a scaled HR platform. The point wasn’t clairvoyance. It was signaling: we’re in the boat.

Eight months after that breakfast, we closed 1517 Fund I at $20M with 30 limited partners. Individuals and family offices, mostly. A lot of international capital. Not a lot of Bay Area “I already see everything” money. And we started writing the earliest checks that we could.

What We Actually Do

1517 is Fellowship 2.0. Our core thesis is that we back founders without college degrees. Carrying forward that mission of proving out that one path is not for all is very important to us and is the bulk of our portfolio. And while that is our focus and mission, wily sci fi scientists starting knocking on our door. Rockets, fusion, quantum computing. They were coming to us because, at the Thiel Foundation, Michael was heading up grants to scientists working on the fringe, so people knew that we were game to hear a crazy idea or three.

It was 2018 and we had one more check to write out of Fund I (into our 43rd company) and that’s when backing sci-fi scientists became our deliberate “thesis breaker,” as brilliant and wild scientists kept showing up. If we were going to deviate, it would be for the kinds of things that make our dropouts proud: making the impossible possible, making science fiction a reality.

Today in Funds III and now Fund IV those circles of our thesis areas have overlapped more and more—young founders reaching for the edge of the impossible, earlier than ever.

We’re most often the first check into a company. Sometimes when it’s just an idea, with $100K for R&D; and sometimes when there’s a semblance of a prototype with a $500K - $1M check. For allocation we look to come in for 7 - 10% depending on the current state of the company.

The role we play the most is that of first believer. And trusted confidant. We also help with hires, connect makers to experienced founders for tactical support, make intros for the next round, and have more of the attitude of the camp counselor over the executive coach. My business card showcases a subtitle of professional fairy godmother and Michael’s antithetical scholar. We both take ourselves very and not very seriously all at once.

With our investors we under-promise and over-perform. Which is turns out is not the norm in the industry. We don’t mark up SAFEs (we only take marks on priced rounds). We keep salaries modest and align our team with carry. We spend money to build our firm bringing in more teammates (5 full time and 10 with part time people) and put capital into community building and events. We try to make our word worth something in an industry where hype trumps substance in the short term.

Funds, Markets, and the 1% That’s Yours

Fundraising has felt wildly different each time and the market explains most of it.

Our fund sizes: $20M → $24M → $80M → now $100M.

2015 - Fund I came together fast. 8 months from first conversations to last close. We were too busy learning to notice the water we were swimming in. But we learned that any LP who talked to one of our fellows, and made an investment in them, would make an investment in us.

2019 - Fund II was a slog. 2.5 years from first conversation to last close. The undercurrent in many a conversation was that maybe we got lucky on a couple deals, but how did we know it was repeatable? We closed at $24M during COVID after originally targeting $40M. Meanwhile, inside the portfolio, Luminar would IPO in December of 2020 (after our last close of Fund II) and return 4X to our investors in Fund I—a gift that changed the conversation for our next fund from being lucky to being brilliant.

Early 2022 - Fund III was fast, four months from first conversation to last close. A year after the Luminar IPO and right before the market rolled over. Investors emailed back “count me in for five/ten,” the unicorn days were in the rearview but still visible, and our numbers were battle-tested. The current was with us. In December of 2023 Loom would be acquired for just shy of $1B and we’d return another 1X to our Fund I investors.

Early 2025 - Fund IV is harder again. Fewer IPOs the last three years. Secondaries are active, public markets are thawing, but LPs are constrained since returns have been scarce over the last three years. In addition, Fund I is clearly one for the books but Funds II and III need more time to bake. Were we “just lucky” with Fund I, is the tension looming in the air. That said, we’ve reached first close and have already made 12 investments into new companies.

The “effort vs timing” lesson has become painfully clear. As a kid who was likely undiagnosed with dyslexia, effort was everything. Without it I would have been held back in first grade and been ridiculed — maybe not outright, since I was a girl and could hide my difficulties by being compliant and kind, but everyone would know that I didn’t matriculate with my peers.

Anyway, effort is one of my super powers: push the boulder uphill, week after week. But having the context of the environment you’re in adds perspective, it’s not only about effort. What is the water you’re swimming in?

Now I think of it as 99% market, 1% you—your job is to give 1000% to the 1% that’s yours. But you can be smart about it and pick your moments. Save some fuel in the tank for the gusts. Our next gust is with Lambda Labs, a Fund I portfolio company that is coming into full fruition. The secondary groups email us eagerly with higher and higher prices.

A marshmallow test like no other, sell now and get one marshmallow! Or wait — and get a bajillion of them. We’re waiting. And so are our LPs (thank you!). But we’re going to make the best damn s’mores the world’s ever seen at our next camp.

On Integrity (And Why It Matters Right Now)

I’ve always seen GP behavior that drives me nuts. The transitional nature, the “what deals do you have for me” posturing, the braggadocio name dropping, the AUM flexing. I’ve gotten used to it — kinda yawn.

But when in a fundraising mode, and the pressure is on, I have to say that it really really frosts my cookies. The manufactured scarcity:“first and last close at once,” then quietly holding the fund open (which is some girl scout level crossies behind the back shenanigans); raising new funds with no intent to deploy in this market; $350k+ GP salaries at small funds; marking up their own SAFEs to look better on paper and skipping out on doing audits.

LPs deserve to know that this is not an apples to apples arena. Many a game are being played.

Ask GPs:

When will you actually deploy capital?

What are your salaries?

What’s your management fee?

Is your “last close” actually your legal last close?

Call the bluffs. As they say in one of my favorite movies of all time “The truth just sounds different.” (Almost Famous, Penny Lane asking William Miller how old he is)

We’ll keep doing it the 1517 way. No FOMO tricks. Conservative accounting. Putting management fees into firm and community building over high GP salaries. Real thesis building and mission critical focus over fads.

And we already have that very real DPI on Fund I of 4.5X and with more to come. Funds II and III have backed some great and world changing companies like Xona Space, Stark Therapeutics, Rainmaker, and Positron. And in the fullness of time, others will see what we saw earlier. It takes time for the market, that big ocean, to catch up to what we saw in a raindrop.

(p.s. AI didn’t write that last line and I’m really proud of it. Maybe I am a writer?!)

Our way is slower, but like the tortoise and the hare, we know who is winning this race.

The Work That Matters

We continue to back dropouts and sci-fi scientists at the earliest stages. We avoid the tool-layer stampede in hype cycles. Fads rotate—Web3, crypto, now AI and humanoid robots—but foundational people endure. Founders with exceptional stories, who are willing to die on their swords to see their vision through and buck today’s systems, that’s who we back.

Our work still feels like education. To me, the best version of VC is early, belief-based, and compounding—time, trust, and small bits of capital at the moment when doubt is loudest. It’s helping someone hold onto a sentence they wrote at 18 years old and making sure the world doesn’t sand it down. It’s telling a founder “you can keep the vision,” like I was told when I started a school with zero administrative experience in the middle of a financial crisis.

I joke that I get to drink from the fountain of youth. It’s not a joke. Every day I meet people audacious enough to try something that might not work yet and is by its very nature “too early.” My job is to give them oxygen, connect them to each other, and protect that spark from the wind long enough to become a fire.

If you’re building from the edges—outside traditional credentials, with a big, maybe-weird idea—our door is open. The current will change ten more times. Your 1% is still yours. And if you bring the mission, we’ll bring the match.

thanks for inspiring all of us, Danielle!

What an inspiring story.